Disclaimer

The information provided in this article is for educational and informational purposes only. It is not intended to be, and should not be construed as, financial, legal, or tax advice. Meristem is not a financial advisor, and the content of this article is not a substitute for professional financial or legal advice. You should consult with a qualified professional before making any financial decisions.

Key Takeaways: Building a Financial Foundation for Your Young Adult’s Future

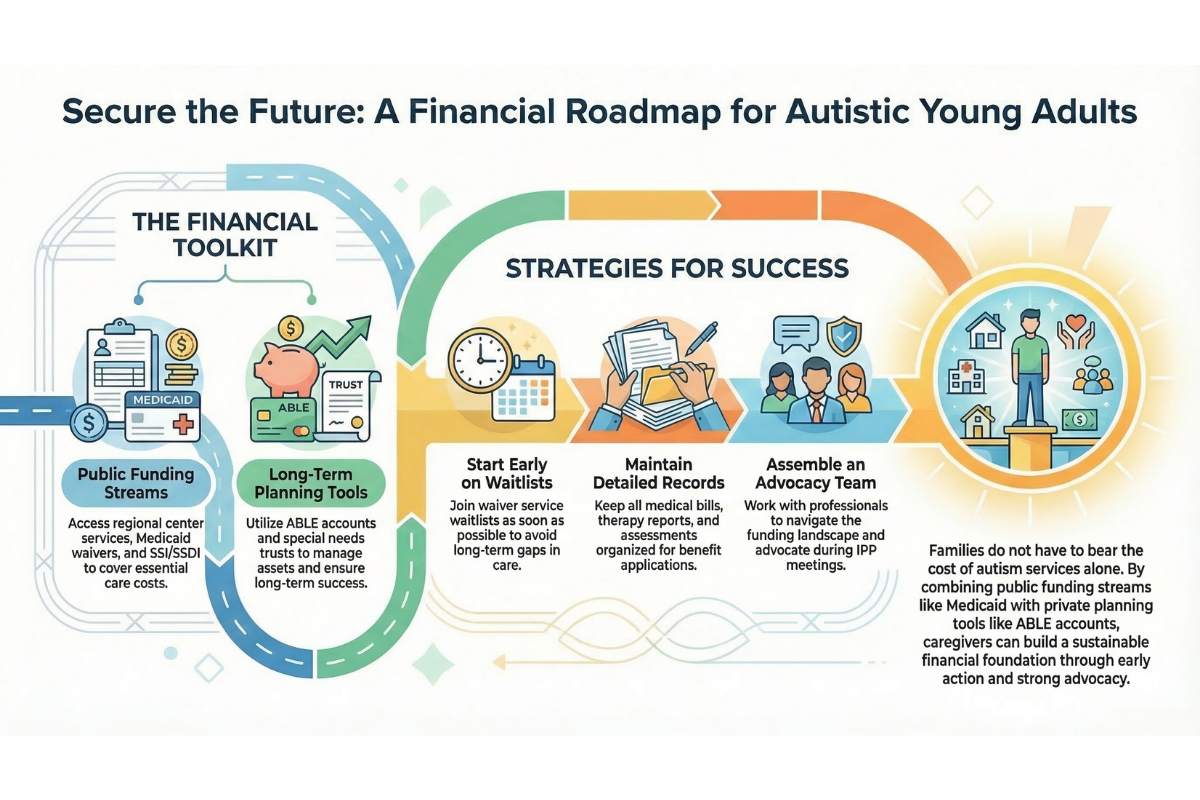

Securing the right services for an autistic young adult is a significant investment in their future. The good news is that you do not have to bear the cost alone. A complex but robust system of public and private autism program funding exists to help families afford the high cost of quality care. This guide will walk you through the primary funding streams, including regional center services, Medicaid waivers, SSI/SSDI, and long-term financial planning tools like ABLE accounts and special needs trusts. Understanding how these pieces fit together is the first step toward building a sustainable financial plan for your young adult’s long-term success.

The Cost of Quality Autism Services: Understanding the Investment

There is no sugarcoating it. The cost of comprehensive transition programs and lifelong support for autistic individuals can be substantial. These costs can include tuition for specialized programs, therapeutic services, housing, and daily living expenses. While the numbers can be daunting, it is important to frame them as an investment in your young adult’s future independence and quality of life. The goal of this guide is to show you how to leverage a variety of funding sources to make that investment possible.

Funding Source 1: Regional Center Purchase of Service (POS)

As we discussed in our companion article on understanding regional center services, California’s regional centers are often the primary source of funding for autism services. If your young adult is a regional center client, the services outlined in their Individual Program Plan (IPP) will be funded through a Purchase of Service (POS) authorization. This means the regional center will pay an approved service provider (a “vendor”) directly for the services your young adult receives.

How it works:

- IPP is Key: The services the regional center will fund are determined by the goals in your young adult’s IPP. If a service is deemed necessary to help them achieve their goals, the regional center is generally obligated to fund it.

- Vendorization: Programs like Meristem become approved vendors with regional centers. This allows the regional center to pay the program directly for tuition and other approved services.

- Payer of Last Resort: The regional center is the “payer of last resort.” This means you must exhaust all other potential funding sources, such as private insurance or school district funding, before the regional center will pay.

Working with your service coordinator to ensure your young adult’s IPP accurately reflects their needs and goals is the most important step in maximizing regional center funding.

Funding Source 2: Medicaid and Home and Community-Based Services (HCBS) Waivers

Medicaid (known as Medi-Cal in California) is a joint federal and state program that provides health insurance to low-income individuals. For many autistic adults, Medi-Cal is a critical source of funding for medical care and other services. Beyond basic health coverage, the most important part of Medicaid for many families is the Home and Community-Based Services (HCBS) waiver program.

HCBS waivers allow states to “waive” certain Medicaid rules to provide a broader range of services to individuals who would otherwise require institutional care (like in a hospital or nursing home). These waivers can fund a wide variety of services, including:

- In-home supports

- Respite care

- Day programs

- Supported employment services

- Environmental modifications

How it works:

- Eligibility: Eligibility for HCBS waivers is typically based on the individual’s income and assets, as well as their level of need. In many cases, the parents’ income is not considered for adult children.

- Waitlists: Because the demand for waiver services often exceeds the available funding, many states have long waitlists. It is crucial to get on the waitlist as early as possible.

- Coordination with Regional Center: In California, many HCBS waiver services are administered through the regional center system. Your service coordinator can help you apply for and coordinate waiver services.

Funding Source 3: Supplemental Security Income (SSI) and Social Security Disability Insurance (SSDI)

SSI and SSDI are two different federal programs administered by the Social Security Administration (SSA) that provide monthly income to individuals with disabilities.

| Program | What It Is | Who Is Eligible |

|---|---|---|

| SSI | A needs-based program that provides a monthly cash benefit to individuals with limited income and resources. | Individuals with disabilities who have never worked or have not worked enough to qualify for SSDI. |

| SSDI | An insurance program that provides a monthly cash benefit to individuals who have a work history and have paid into the Social Security system. | Individuals with disabilities who have a qualifying work history, or who are the adult child of a retired, disabled, or deceased worker. |

For many autistic young adults, SSI is the more common benefit. The 2026 federal benefit rate is $994 per month for an individual, though this amount may be reduced based on other income. It is important to note that there are strict income and asset limits to maintain SSI eligibility. The Student Earned Income Exclusion (SEIE) allows a student under age 22 to earn up to a certain amount without it counting against their SSI benefits, which can be a powerful tool for encouraging work experience.

Funding Source 4: ABLE Accounts and Special Needs Trusts

One of the biggest challenges for families is how to save for their young adult’s future without jeopardizing their eligibility for needs-based government benefits like SSI and Medicaid. Two key tools for this are ABLE accounts and special needs trusts.

ABLE Accounts:

An ABLE (Achieving a Better Life Experience) account is a tax-advantaged savings account that allows individuals with disabilities to save money without it counting against their asset limits for government benefits. In 2026, up to $19,000 per year can be contributed to an ABLE account. The money can be used for a wide variety of qualified disability expenses, including education, housing, transportation, and healthcare.

Special Needs Trusts (SNTs):

A special needs trust is a legal arrangement that allows a person with a disability to hold assets in a trust for their benefit. The assets in the trust are managed by a trustee and can be used to pay for a wide variety of expenses that are not covered by government benefits. Because the individual does not own the assets in the trust directly, they do not count against their asset limits for programs like SSI and Medicaid. SNTs are more complex and expensive to set up than ABLE accounts, but they can hold a much larger amount of assets and offer more flexibility.

Funding Source 5: Scholarships and Grants

While less common than other funding sources, there are a number of scholarships and grants available specifically for autistic students. These can be a valuable source of funding for college, vocational training, or other post-secondary programs. Some organizations that offer scholarships include:

- The Organization for Autism Research (OAR): OAR offers several scholarships for autistic students pursuing post-secondary education.

- The Schwallie Family Scholarship:This scholarship supports students with ASD pursuing undergraduate education.

- The Lisa Higgins Hussman Scholarship: This scholarship is for autistic students pursuing degrees or certificates at two-year or four-year colleges.

It is also worth researching local community foundations and service organizations, which may offer scholarships for students with disabilities in your area. Websites like Scholarships.com and Bold.org are excellent resources for finding a wide range of disability-related scholarships.

Funding Source 6: Private Pay and Family Resources

For many families, a portion of the cost of autism services will be paid for out-of-pocket. This can come from a variety of sources, including:

- Family savings and investments

- Contributions from grandparents or other family members

- Home equity lines of credit

- Life insurance policies

It is important to work with a financial planner who specializes in special needs planning to develop a long-term financial strategy that takes into account all of your family’s resources and goals.

Combining Funding Sources for Comprehensive Support

The key to funding a comprehensive transition program is to “braid” together multiple funding sources. It is rare for a single source to cover all of the costs. A typical funding plan might look something like this:

| Service | Primary Funding Source | Secondary Funding Source |

|---|---|---|

| Program Tuition | Regional Center POS | Private Pay |

| Therapy Services | Private Insurance | Medicaid Waiver |

| Living Expenses | SSI/SSDI | ABLE Account |

| Recreation | Family Resources | Scholarships |

Financial Planning for Long-Term Needs

Financial planning for a child with a disability is a lifelong process. It is important to start early and to work with a team of professionals who can help you navigate the complex legal and financial landscape. This team might include:

- A special needs financial planner

- A special needs attorney

- A tax advisor

These professionals can help you with a variety of tasks, including:

- Creating a long-term financial plan

- Setting up a special needs trust

- Navigating the complex rules of government benefits programs

- Planning for your own retirement while ensuring your child’s long-term financial security

Understanding Program Costs and What’s Included

When evaluating programs, it is crucial to understand the full cost of attendance and what is included in the tuition. Some programs may have a single, all-inclusive fee, while others may have a base tuition with additional fees for services like therapy, transportation, or community outings. Be sure to ask for a detailed breakdown of all costs and fees so you can make an informed decision.

Maximizing Available Funding

Here are a few tips for maximizing the funding available to your family:

- Start early: Get on waitlists for waiver services as soon as possible.

- Keep good records: Keep detailed records of all of your child’s expenses, including medical bills, therapy reports, and educational assessments. This will be helpful when applying for benefits and services.

- Be a strong advocate: Do not be afraid to advocate for your child’s needs in IPP meetings and with other service providers. The law is on your side, but you have to be prepared to make your case.

- Work with a team: Assemble a team of professionals who can help you navigate the funding landscape. This may include a special needs attorney, a financial planner, and an advocate from a local disability rights organization.

- Explore all options: Do not assume that you are not eligible for a particular program or benefit. The rules are complex and often change. It is always worth applying.

Tax Deductions and Credits for Disability-Related Expenses

There are a number of tax deductions and credits that may be available to families of individuals with disabilities. According to IRS Publication 502, you may be able to deduct the cost of unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI). This can include the cost of diagnostic services, therapeutic services, and even tuition for a special school if the primary purpose of the school is to provide medical care. For example, if your AGI is $100,000, you can deduct medical expenses over $7,500. If you have $10,000 in qualifying expenses, you can deduct $2,500.

Other potential tax benefits include:

- Earned Income Tax Credit (EITC): If your adult child has a disability and is working, they may be eligible for the EITC.

- ABLE Account Tax Credit: Some states offer a state tax credit for contributions to an ABLE account.

It is important to work with a tax advisor who is familiar with the tax laws related to disability to ensure you are taking advantage of all of the deductions and credits available to you.

Working with Financial Planners Who Specialize in Special Needs

Working with a financial planner who specializes in special needs can be a game-changer for families. These professionals, who often hold designations like the Chartered Special Needs Consultant (ChSNC®), have a deep understanding of the unique financial challenges that families of individuals with disabilities face. They can help you with a variety of tasks, including:

- Creating a comprehensive financial plan that integrates all of your family’s resources and goals

- Setting up and managing a special needs trust

- Navigating the complex rules of government benefits programs to avoid jeopardizing eligibility

- Planning for your own retirement while ensuring your child’s long-term financial security

When interviewing potential planners, be sure to ask about their experience with special needs planning, their qualifications, and their fee structure. You can find qualified professionals through the Special Needs Alliance or by searching the FINRA BrokerCheck database for advisors with the ChSNC® designation.

How Meristem Works with Various Funding Sources

At Meristem, we understand that navigating the funding landscape can be overwhelming. Our admissions team works closely with families to explore all available funding options and to create a customized financial plan. We are an approved vendor with many California regional centers, and we work with families to coordinate regional center funding, private pay, and other resources.

Our goal is to make our life-changing programs as accessible as possible to all families. We believe that with the right planning and support, every young adult can have the opportunity to reach their full potential.

Discuss Funding Options

If you have questions about funding options for your young adult, we encourage you to schedule a consultation with our admissions team. We are here to help you navigate the process and to create a plan that works for your family.

Voices of Community Podcast

Join us for conversations with autistic adults, families, and professionals who are helping shape a more inclusive world. Each episode shares personal stories, insights, and perspectives from across the Meristem community and beyond.